Sparkling wines

In 2015 the world trade of sparkling wines kept on growing: the aggregate of the 10 major exporting countries makes up a volume of almost 7 million hectolitres, grown by 7% versus 2014, for a total value of 5.1 billion US dollars, which accounts for a yearly -6%, however including the strong appreciation of the American currency to the Euro and other currencies: net of the exchange rates, the figure is instead to be considered on the rise by at least 10%. In this way we also have to read all other negative data, in the column of values for the different countries and of the relevant average prices, which resulted to be decreasing.

In the leading trio including Italy, France and Spain, especially the first two countries are driving: thanks to Prosecco, Italy increases its volumes by 15%, reaching a 40% share on the total aggregated amount of the 10 countries. France is also growing well, benefitting from the recovery of Champagne, definitively out of the recession experienced between 2009 and 2012. On the contrary, the Cava driving force is at a standstill, after 4 years of uninterrupted growth, registering a balance in the exported volumes, at 1.7 million hectolitres. This was caused, among other things, by the slowdown of the Belgian market, one of the main destination markets of the products made in Spain.

The year was negative for the German sparkling wines, closing at -10%, whereas the more and more successful South-African products, jumped over 13 million litres, corresponding to a yearly rise of 35%.

In the long-term (2004/15), the US dollar trend penalizes the calculation based on 2015, but however Italy recorded a cumulated 12% growth, against a scarce +3% of Champagne and Cava wines.

On the import front, aided by the booster Prosecco and by the recent recovery of Champagne shipments, the USA and the UK are stabilizing as the major destinations of sparkling wines in the world, with a total of almost 2 billion US dollars. The recent decreases in the German market are instead favouring the overtaking of Japan, gone up to third position, with a five-year growth of 6%.

Bottled wines

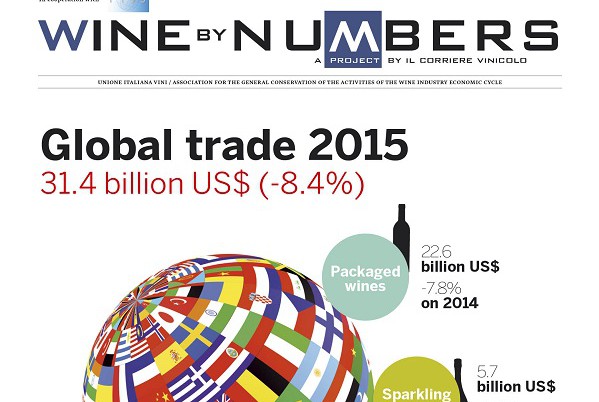

The year 2015 saw a general slowdown in the value of world trade exchanges of bottled wine (excluding sparkling wines): the total amount went below 23 billion US dollars (precisely 22.6), aided by the appreciation of the US Dollar to the Euro, reference currency of the major European manufacturers, which, on the other hand, enabled a certain revitalization in volumes.

Considering values, France remains the first largest world supplier (Italy is the leading supplier with regard to volumes worldwide). The French wines started to accelerate again with Bordeaux, recovering on the Asian front after a terrible 2014. The Italian growth in value is moderate and so is the Spanish one. The big players of 2015 are Chile, which found large market in Asia thanks to free trade agreements and tax breaks (China, Japan), and New Zealand, which is having very good results in the USA and in the Far East. Argentina and South Africa are stable, whereas Australia compensated the decreases in the UK and in the USA with very high performances in China and in the Asian area.

In the long-term, splitting the decade 2004/15 in two halves, the Old and the New Worlds encountered similar regressions: from an over +4% growth in 2004/09 to a limited +1% in the following five years, which should have brought a recovery and was actually weakened by the currency trend. The grand total world trade halves the increasing trend between the two periods, from an almost +5% to a +2%.

Observing the charts of the annual developments, we are tempted to say that the expansion movement, triggered after 2009, shows signs of extended stability now. If it is true that the Old World’s currency dynamics enhanced the decline of the trend, it is also true that in the last two years the situation was rather flat. The same standstill situation was registered in the New World in the last four years, where there has been no growth since 2011.

In consideration of these trends, the pie chart shows a decrease of the European shares, at 59%, -6 percentage points in 11 years’ time, whereas the representatives of the New World remain stable, at a little less than 1/3. On the contrary, the Rest-of-the-World countries registered a growth, reaching almost 3 billion US dollars in 2015, with a moderate +7% CAGR between 2010 and 2015, only one point lower than 2009/14.

With regard to imports, the United States – also thanks to the positive trend of the USD/EUR exchange rate experienced – increased their importance as absolute leaders, with a value of imported wine exceeding 4.1 billion US dollars. Great Britain is stable at 2.9 billion, whereas China – thanks to an extraordinarily important year – jumped over Germany, confirming its third place in the ranking of worldwide importers, with a five-year 23% upturn.

Bulk wine

In 2015 the world export of bulk wine broke a new record in volume: the aggregate of the major producing countries reached 36.3 million hectolitres, thus increasing by 3% versus 2014. A slowdown in the value of exchanges is also shown, linked to the currency movements as seen for bottled and sparkling wines (3.1 billion US dollars, -13.7% on 2014).

The growth was driven by Spain, world leader (+10%, at 14 million hectolitres) and Chile (+15%, at 3.7 million), whereas decreases were reported in Italy (-13% at 4.8 million) and in France (-9%).

The two aggregates Old and New Worlds had diversified increase performances, both in the short and in the long term: in 2015 Europe scored a 1% growth versus 2014, reaching 22.3 million hectolitres, whereas the aggregate of the New World countries almost attained 14 million hectolitres, with an annual increase of 7%. In the long term (from 2003 on), there was a stronger trend in Australia, Chile, Argentina and in other countries, at a cumulated +10%, whereas the Europeans reported only a 3% growth.

With regard to imports, two completely different markets, such as the UK (first supplier Australia, mainly branded wines) and Germany (first supplier Spain, wines for sparkling-wine bases) totalled 1 billion US dollars of import value, remarkably outpacing the USA and France. A strong downturn was recorded in Russia, overtaken even by Belgium.